Tokemak

Introduction 👋

This is the first article in our Protocol Analysis series. In this series, we use our investment template outlined in How to Analyse a Web3 Protocol to fundamentally and critically analyse a variety of crypto protocols, aiming to separate the ‘real’ from the hype. Let’s dive in!

Protocol: Tokemak, a decentralised market maker that aims to create a ‘liquidity infrastructure layer’ for DAOs, DeFi projects, market makers, and exchanges.

Overview of Tokemak 🗒️

Within the Web3 value stack, Tokemak sits within the broader realm of DeFi, and can be described as a decentralised market maker. It also holds a unique place in the Metagovernance space – which refers to holding one DAO’s token in order to influence decisions in another DAO(s), a concept popularised by the Curve Wars. At a high level, Tokemak enables holders of the TOKE token to apportion liquidity to a variety of different exchanges – but there’s a lot more detail around how Tokemak works that we’ll cover.

It is built on Ethereum, but is planning on being a multi-chain protocol, which is encouraging if you believe in a multi-chain future; a protocol built across blockchains, which provides liquidity across chains and exchanges, has a much larger addressable market. Moreover, Tokemak has raised $4 million from the likes of Framework Ventures, Electric Capital, Coinbase Ventures, North Island Ventures, Delphi Ventures, and ConsenSys. These are all reputable VC firms, which grants some level of comfort and although the funding is on the lower side, as we’ll see, the team has managed to do quite a lot with the investment.

Tokemak sees liquidity as the most critical infrastructure of the token ecosystem, since without deep liquidity, it is difficult for any token to survive – indeed, a lot of DeFi projects we’ve seen have been variations on trying to bootstrap enough liquidity to their own ecosystems. Tokemak’s long-term goal, therefore, is to become the primary decentralised liquidity provider across the Web3 ecosystem by providing Liquidity-as-a-Service to all types of Web3 projects.

How Does Tokemak Work? 🤷

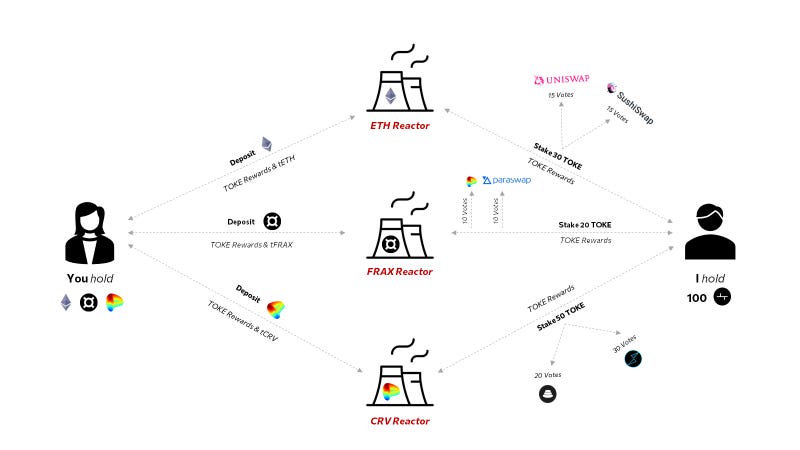

The traditional way of providing liquidity is by adding liquidity to a ‘pool’ that consists of two equally balanced assets. In Tokemak’s spin on this model, each asset supported by Tokemak has its own ‘Token Reactor’. A liquidity provider (LP) deposits tokens into the token reactor, and a liquidity director (LD) stakes TOKE and is able to vote on which exchanges that liquidity is allocated to. Moreover, as TOKE holders, LDs have a pro-rata claim on the treasury of protocol-controlled assets (PCA).

Let’s say run through an example.

Assume you hold ETH, CRV, and FRAX. You, as a liquidity provider, deposit the ETH into the ETH Token Reactor, CRV into the CRV reactor, and FRAX into the FRAX reactor. In return, you obtain:

A liquid derivative of the deposited asset – a tAsset, a bearer asset that represents a tokenised claim on the underlying asset. So, you get tETH, tFRAX, and tCRV.

TOKE rewards.

Then, assume I hold 100 TOKE. I stake that TOKE and obtain 100 votes. I choose to allocate 30 votes to ETH, 50 votes to CRV, and 20 votes to FRAX.

I can then choose to allocate the TOKE I have staked to each reactor to particular exchanges. The liquidity is directed towards a particular exchange in one-week cycles. My voting power in each reactor is proportional to my share of the total TOKE staked to the reactor. Let’s see how I could allocate my votes:

30 ETH votes: I allocate 15 votes to Uniswap and 15 votes to SushiSwap.

20 FRAX votes: I allocate 10 votes to Paraswap and 10 votes to Curve.

50 CRV votes: I allocate 20 votes to Balancer and 30 votes to Thorswap.

The below diagram may be helpful:

The defining feature of Tokemak is its single-sided liquidity. Instead of needing to balance two separate assets and go through the complexities of interacting with a DEX, Tokemak makes it easy for LPs to deposit a single asset and, at the same time, be protected from impermanent loss (IL), which is instead borne by LDs. LPs are protected from IL since they do not have to pair their asset with another asset, i.e., they get out what they put in. Since LDs must stake TOKE, they are exposed to the price volatility of two assets (TOKE and the reactor asset), and thus have to bear IL.

All reactors are intended to be balanced, i.e., the ratio between the LP deposits and the TOKE staked by LDs is meant to be as close to 1:1 as possible. To incentivise this, the protocol adjusts the interest rate paid out to LPs and LDs in the following manner; when:

The value of assets within a reactor > value of TOKE staked, the protocol increases the interest rate paid to LDs to incentivise more TOKE deposits;

The value of assets within a reactor < value of TOKE staked, the protocol increases the interest rate paid to LPs to incentivise more asset deposits.

The last piece of the puzzle is the Pricers, who provide real-time pricing information for any protocol that does not use an Automated Market Maker (AMM). Pricers set buy and sell order prices in this case, and use a separate pool of Tokemak assets to maintain the asset’s market.

All fees generated from providing liquidity on DEXs are retained by the Tokemak treasury.

The Trends Supporting Tokemak’s Emergence 📈

Problems of Liquidity Mining

DeFi 1.0 and DeFi Summer were characterised by liquidity mining, which, as we highlighted in What’s Catching My Eye in DeFi, is extremely unsustainable:

As we’ve seen, though, liquidity mining has proven to be unsustainable. Its inflation-based tokenomics has led to the kings of DeFi Summer, such as Compound, being brought to their knees. Compound, for example, distributed more than $300 million in token incentives from June 2020 to September 2021, and earned ~$34 million in protocol revenues over the same period. Even if the liquidity mining program can be chalked off as a customer acquisition cost (CAC), Compound has earned only an additional ~$15 million in revenues between October 2021 (when the program ended) and March 2022, at an average of ~$2.5 million per month.

Capital in DeFi is also mercenary. It is perpetually searching for the highest risk-adjusted yield, and most high yields are a form of CAC and can be attributed to token rewards. When these decrease or end, capital leaves to hungrily find the next opportunity. The way liquidity is attained within DeFi today is fundamentally unsustainable and unscalable – it is too risky and costly, and there is a need for an improved solution.

Metagovernance

The Curve Wars has been one of the main facets of DeFi 2.0, and has spawned the concept of metagovernance, where a protocol (e.g., Convex, CVX) holds the governance tokens of another protocol (e.g., Curve, CRV) in order to influence Curve emissions (which essentially provide deep liquidity to stablecoins). Holding Tokemak’s TOKE could similarly enable DAOs, DeFi protocols, and basically all types of Web3 protocols that have tokens, to increase the liquidity of their tokens across various exchanges and trading venues.

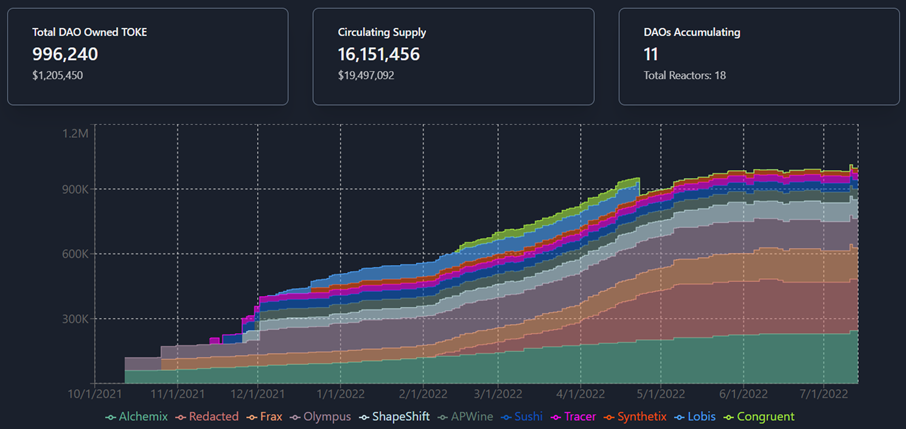

Indeed, the Toke Wars Dashboard represents how DAOs have been accumulating TOKE over time:

Being cross-chain definitely helps with Tokemak’s ambition to enable as many protocols as possible to accumulate its token. There’s also a gap in the metagovernance market for a Convex-like protocol that attempts to hold as much TOKE as possible – this could provide more fuel to Tokemak’s adoption across Web3.

Launch, Traction, and Future Roadmap 🚀

At launch in August 2021, participants exchanged ETH or USDC for TOKE, which enabled Tokemak to start building its treasury of protocol-controlled assets. They were also able to acquire ‘base’ assets to be paired with reactor assets when liquidity is directed to an exchange.

The list of protocols with Tokemak reactors to date are:

Phase 1: FRAX, Alchemix, Tracer DAO, Olympus DAO, SushiSwap

Phase 2: ShapeShift, Visor, Synthetix, Illuvium, AP Wine

Phase 3: DODO, [REDCATED] Cartel, Silo Finance, BitDAO, Rook

Over the long-term, Tokemak wants to accumulate enough trading fees in order to direct liquidity independently without the need for LPs. The end-game is for Tokemak to be self-sufficient, a point which is referred to as the ‘Singularity’.

Team 🤵♂️🤵♀️

Tokemak’s founder is Carson Cook, who has a master’s degree in Electrical Engineering, a PhD in Physics, and is ex-McKinsey. His previous experience is pertinent – he was the founder of Fractal, a cryptocurrency trading and technology firm that provided a proprietary algorithmic trading platform for digital assets and used algorithmic strategies to offer liquidity. In 2018, Cook was a market maker on centralised exchanges and moved to DEXs towards the end of the year. Cook’s prior experience in the liquidity provisioning field is a positive and having been involved in the market making space for a while, it’s interesting to see how he and his team are attempting to disrupt the market making ecosystem. Cook and his team are also not anons, giving them more skin in the game.

Another noteworthy team member is @0xMaki, the co-founder of SushiSwap, who joined Tokemak as its chief strategy advisor. Getting an experienced hand on board may be helpful in steering the project in the right direction, although the manner in which @0xMaki departed SushiSwap and its subsequent struggles compared to Uniswap indicate that this isn’t a sure-shot success.

Use Cases 💡

Protocols & DAOs

Protocols today, especially DeFi ones, spend inordinately long on liquidity issues. DeFi project founders spend between 25% and 75% of their time on these issues, where their attention could be utilised much better elsewhere. Projects also pay an average of $1.25 per $1 of liquidity sourced. Carson Cook says this figure could be reduced by 3-4 times through Tokemak, which, if he’s right (which is to be proven) is a powerful incentive for projects to accumulate TOKE.

DAOs also have a lot of their own native tokens that are locked and vesting in their treasury. They can provide these assets as LPs into Tokemak, while simultaneously earning rewards in TOKE and direct the flow of its own liquidity to exchanges, enabling its token to attain liquidity across a range of venues. In return, DAOs receive tAssets that they can hold in their treasury.

Stablecoin Issuers

Stablecoin issuers could use Tokemak to pair their stablecoins with base assets like ETH on DEXs, ensuring deep liquidity for their stablecoins on DEXs.

DEXs

Tokemak acts as a hose which directs liquidity to DEXs. More liquidity means better pricing and less slippage, driving up trading volume and fees.

Tokenomics 💸

Value Accrual

The TOKE token has four key aspects:

Enabling governance over the Tokemak DAO, which controls the treasury;

Providing incentives for LPs, LDs, and asset depositing;

Provides a backstop if impermanent loss gets too high;

Directing liquidity to trading venues.

TOKE is meant to be held by a wide variety of entities and given that supply of TOKE is capped at 100 million, this can potentially make it a valuable resource akin to a commodity for those entities.

Overall, Tokemak accrues value and generates revenue via:

The trading fees it earns from exchanges, all of which goes into its treasury;

Liquidity rewards;

Depositing idle assets to protocols like Compound and Aave (this will depend on the risk factor of the protocol that is deposited into, as shown by the travails of Three Arrows Capital and Celsius recently).

Token Release

5,600 TOKE per day for LPs in token reactors (project tokens);

2,820 TOKE per day for LPs in pair reactors (stables and ETH);

4,900 TOKE per day for LDs;

The emissions schedule for protocol participants of 30 million TOKE is currently designed to be emitted over 24 months; however, this is not set in stone, and could extend. This indicates that they ideally want to build their treasury up over 2 years, but as we’ll see below, this may be a bit too optimistic.

The token isn’t especially inflationary, and its fixed supply of 100 million potentially means that it is aiming to control token inflation over the long term.

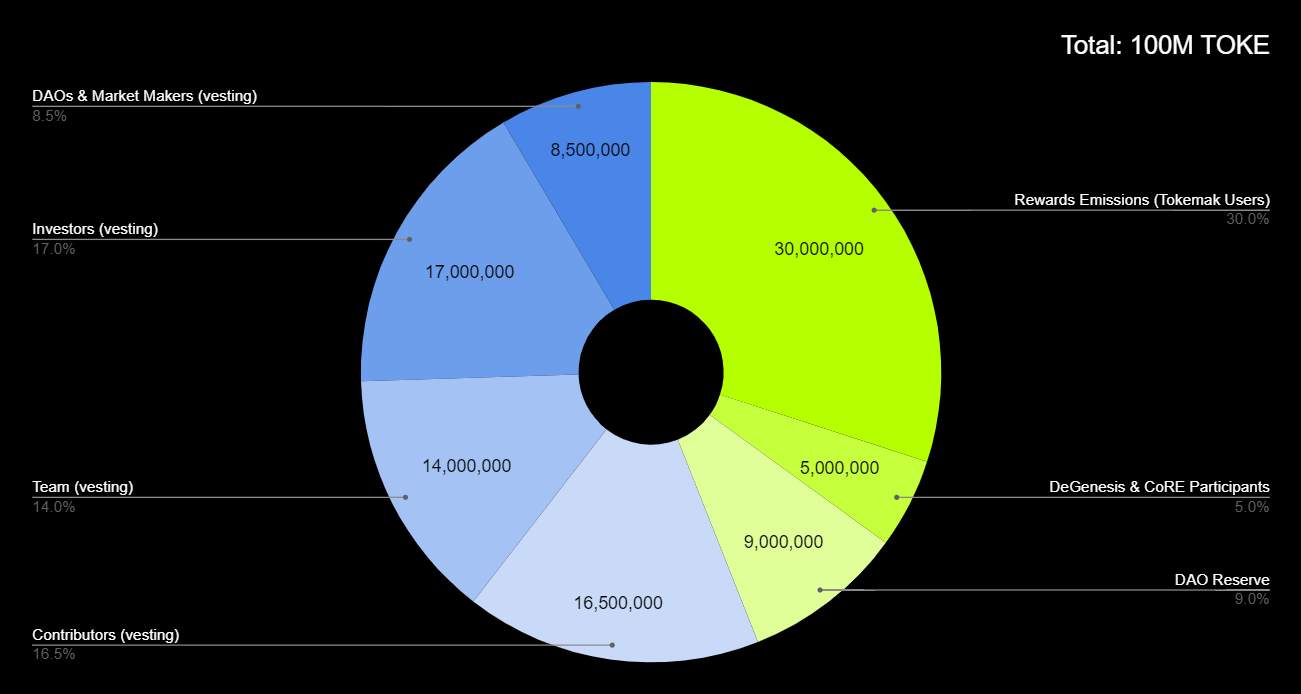

Token Distribution & Vesting Schedule

The below chart shows TOKE’s token distribution:

Contributors, the core team, investors, DAOs, and market makers all have a 12-month cliff and a 12-month vesting period, indicating that supply will start unlocking from August 2022 onwards. This could place (more) downward pressure on the price and add sell pressure, although the hugely diminished token price over the last few months could mean a period of HODLing for a number of stakeholders. However, investors could still want to get rid of TOKE since it is a highly risky asset in an increasingly very risk-off environment.

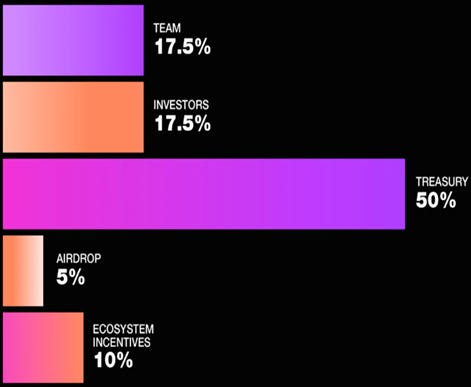

As Cooper Turley and Lauren Stephanian have outlined, a model for optimal token distribution is as follows:

Comparing Tokemak to this model, there are a few key takeaways:

For Tokemak, ecosystem incentives comprise 35%, until which point Tokemak will expect to have enough PCA to provide liquidity without depending on LPs. This is a deviation from the above distribution but seems apt for Tokemak given its longer-term model. It remains to be seen whether Tokemak will adjust this percentage or decide to increase its supply in the future – if it doesn’t, it may have to find another way of attracting LPs to deposit their tokens into reactors.

The amount held in the treasury is only 9% which is much lower than the 50% in the optimal distribution. However, this is caveated by the fact that the reserve/treasury will build up over time and can be viewed in conjunction with the reward emissions since these are aimed to be staked in the reactors.

The distribution for the team is higher than that in the suggested distribution, but 14% is reserved for the core team which is in line with the suggested distribution. The definition of contributors is not clear, which makes it seem like there is more TOKE reserved for the ‘Team’ than may be necessary, and this could be allocated to the treasury or towards building up the treasury over the longer term.

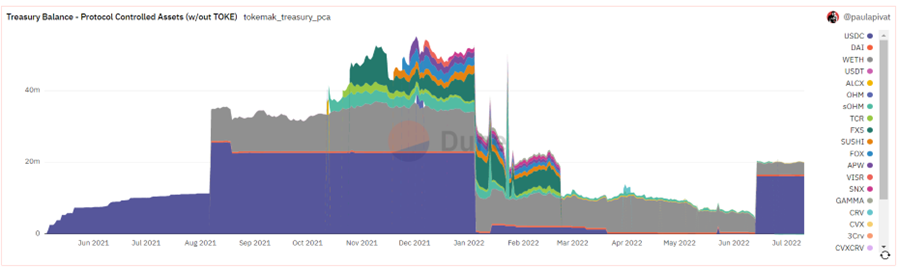

Compared to its protocol revenue, a cumulative total of $6.8 million as of July 2022, and its protocol-controlled assets, which amount to $24 million, as shown below, Tokemak has distributed a staggering $429 million in token incentives.

Tokemak’s tokenomics depend too heavily on incentivising LPs to deposit their assets into the reactors. The mismatch between the token incentives distributed and protocol revenue / PCA needs to be resolved in order to be sustainable in the long-term. Therefore, to attain its goal of being self-sufficient, due to the volatility of the crypto market, it will need to generate far more value in its treasury over the next few years while potentially needing to revamp its tokenomics model, which may prove to be a difficult task.

Governance ⚖️

Tokemak’s governance is not extremely well-established yet, but they have established a governance channel in the Discord over the last few months. In the long-term, when the Singularity is meant to occur, control of the protocol will be transferred to the Tokemak DAO. To improve its governance procedures, Tokemak aims to build out its governance structure, starting with Discord, and it is a good sign it has already started to do so. Tokemak aims to let TOKE governance vote on issues like new reactors, new exchanges, or new chains to implement on.

Performance 📉

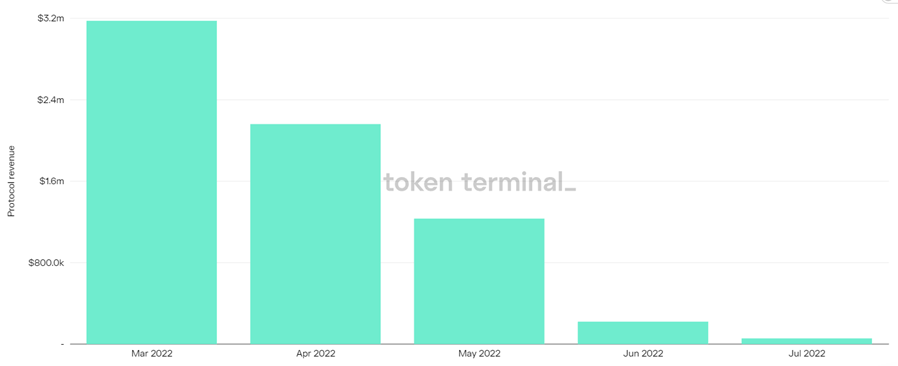

Tokemak’s protocol revenue has cratered over the last 2-3 months of a brutal bear market. As the price of all crypto assets have crashed, a lot of liquidity has vanished from the market and a lot of projects are struggling and just attempting to survive. Therefore, it is expected that these protocols do not have excess cash on hand to hold TOKE and attempt to shore up their own liquidity.

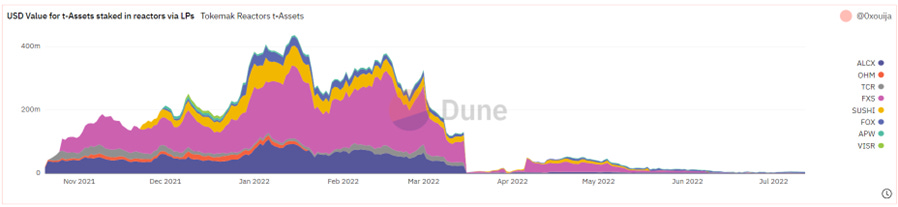

Another statistic directly correlated to the drop in protocol revenue is the amount of t-Assets staked in reactors by LPs. As we can see below, the value of assets staked has fallen off a cliff and has begun to flatline. This will need to significantly pick up – if no assets are staked, then they aren’t traded on DEXs, trading fees don’t accumulate, and Tokemak doesn’t earn any revenue.

Since its high in Nov 2021, moreover, Tokemak’s price has dropped by 98%, and its trading volume has plummeted as well. The growth in the number of token holders has plateaued since January as well – from August 2021 to January 2022, the number of token holders increased by 202%, but this number has increased only 25% since.

Closing Thoughts ⌛

Tokemak’s idea of being the liquidity infrastructure layer for Web3 is heady, and the way in which it is tackling the liquidity problem is ingenious. Its concept as a protocol, its team, investors, and potential use cases are all positives. However, the bear market and its abject recent performance have exposed a flaw in its tokenomics – namely, that it seems to rely too much on token incentives (i.e., emissions that inflated the supply) to liquidity providers, at least in its first 12 months. When these incentives disappear, as they seem to have done recently, capital can desert the system. If this happens before Tokemak is able to generate a substantial treasury of protocol-controlled assets, it could prove to be fatal. This indicates that Tokemak needs to work on improving its tokenomics model to be more sustainable long-term. Namely, the question Tokemak needs to answer is this:

How can we ensure that deposits into a Reactor from Liquidity Providers are sticky, i.e., how do we ensure that capital is not only attracted to the system by token emissions?

To join this journey into the worlds of tech, business, and Web3, subscribe below!

Disclaimer

This is a personal blog. Any views or opinions represented in this blog are personal and belong solely to the article authors and do not represent those of people, institutions or organizations that those authors may or may not be associated with in professional or personal capacity, unless explicitly stated. All content provided on this blog is for informational purposes only. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

👇🏽 please hit the ♥️ button below if you enjoyed this post.