Nexus Mutual

Introduction 👋

This is the seventh article in our Protocol Analysis series. In this series, we use our investment template outlined in How to Analyse a Web3 Protocol to fundamentally and critically analyse a variety of crypto protocols, aiming to separate the ‘real’ from the hype. Let’s dive in!

Protocol: Nexus Mutual, a decentralised insurance protocol that, by means of a blockchain, has created a risk-sharing pool in the form of a mutual to return the power of insurance to the people. The model uses a self-contained tokenomic system to incentivise its members to participate in in Risk Assessment, Claims Assessment and Governance.

Overview of Nexus Mutual 🗒️

Nexus Mutual is a decentralised alternative to insurance built on Ethereum that allows its members to pool their resources and offer insurance for a variety of products – Protocol Cover, Custody Cover, ETH2 Staking Cover, and Yield Token Cover. Launched in 2019, Nexus operates under a ‘discretionary mutual structure’ that gives members a legal right to proportionally own the mutual and enables them to trade with each other under one legal structure.

To date, Nexus Mutual has raised $3 million in funding from the likes of 1confirmation, Blockchain Capital, version one, Semantic Ventures, Kenetic, KR1, Collider Ventures, and 1kx. This is a relatively small amount and is a good sign that the protocol has grown as much as it has without large funding. Nexus currently provides cover for 122 products across multiple protocols, has had its smart contracts audited 3 times – April 2019, June 2020, and May 2021 – and is part of the Immunefi Bug Bounty Programme, indicating that it gives security the requisite level of importance.

Nexus is targeted towards 3 main types of entities:

Projects deploying code that purchase cover to protect against any mishaps.

Individual users of protocols.

Multi-sig wallet contracts, giving them greater confidence in their funds’ safety.

How Does Nexus Mutual Work? 🤷

To join the mutual, members pay a nominal membership fee of 0.002 ETH and complete a KYC/AML process. The KYC process links an Ethereum address to the member, with none of the Personally Identifying Information (PII) being held on-chain. They must then buy NXM tokens in exchange for ETH or DAI, which give them proportional power to run the mutual, judge claims, assess the risk of providing cover, and vote on proposals. To purchase cover, members buy and use NXM tokens, with 90% of the tokens used burned and the remaining 10% locked for the cover period + 35 days, since they are used to submit a claim. Only members will be able to hold tokens, meaning that they cannot be transferred to any Ethereum address that is not marked as a member.

Some core components of Nexus Mutual’s model that we’ll dive into are:

Risk Assessment

Claims Assessment

Capital Model

Asset Investment

Risk Assessment

Risk assessors stake NXM against products they believe are safe, trustworthy, and have bug-free code. Listing a new product on Nexus requires assessors to stake NXM to enable cover to be offered for that product while also bringing down the cost of cover. Essentially, the more NXM staked by risk assessors against a product, the higher the total amount of cover offered and the lower the premium. Nexus allows members to stake against protocols with leverage by holding the NXM in the capital pool as a representation of their membership while simultaneously acting as capital to back products.

When cover is sold on a product, risk assessors earn proportional rewards in NXM equivalent to 50% of the cover premium. When a claim is accepted for a product that a risk assessor has staked against, their staked NXM is proportionally used to provide capital for the payout of the claim. If there is an early claim, then part or all of the stake will be lost.

Nexus places capacity limits on the amount of cover available on specific risks, which provide protection against concentrated exposure to any one type of risk. There are two limits, the lower of which applies in each case:

A Specific Risk Limit based on the amount of staking on a particular risk. If there is no staking against a product, Nexus cannot offer any cover against that risk.

A Global Capacity Limit based on the overall capital resources of the mutual that ensures that Nexus is not overly exposed to a particular risk.

Two other key points to note:

NXM can be unstaked at any time subject to a 30-day withdrawal period.

To avoid the cold start problem, protocols or custodians offering new products can use ‘Shield Mining’, a process that incentivises risk assessors to stake against their product by offering additional NXM or wETH rewards. This opens up cover availability for their products and reduces the premium, incentivising their users to buy cover.

Claims Assessment

Claims assessors stake NXM in order to assess claims, which they do in two ways: using an oracle to provide off-chain data, or crowd-sourcing information via voting mechanics. A member can submit a claim by staking 5% of the NXM tokens that were locked while purchasing cover, meaning that a member can submit a claim twice. If the claim is accepted, the deposit is returned, otherwise it is burned.

The total voting power to assess a claim must be >5x the cover amount, where voting power is determined by the number of staked tokens used to vote. Voting with the consensus gives assessors a share of the fee (premium) pool, paid in NXM tokens and valued at a fixed percentage of the cost of cover. On the other hand, voting against the consensus results in members’ stake being locked for longer – Nexus does not want to burn the tokens since they do not want to disincentivise genuine differences of opinion, and burning may make members wary of assessing claims. No consensus results in a reduced fee pool for assessors and the claim is then escalated to all members for a vote.

One of the most critical aspects of claims assessment is ensuring that legitimate claims are not denied. Nexus has tested its claims assessment design with Incentivai, who use machine learning algorithms to model parameters which “give confidence that close to 100% of genuine claims will be paid and close to 0% of non-genuine claims will be paid”. How exactly this is done is not clear, but it is encouraging that Nexus has thought of and seemingly addressed this problem already.

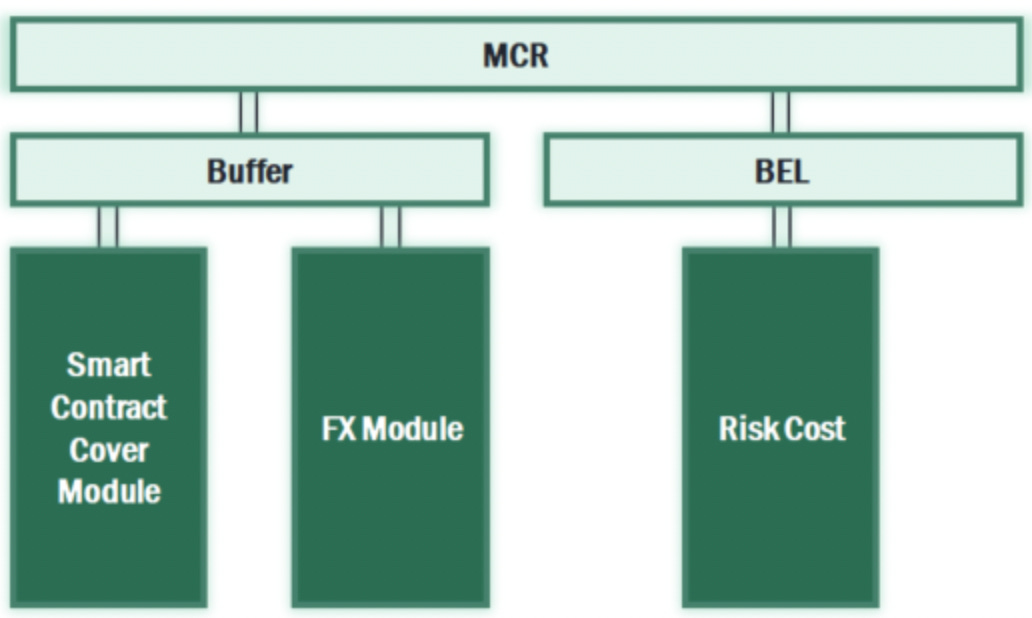

Capital Model

Nexus Mutual’s capital model is built on the insurance-industry standard EIOPA Solvency II methodology that is calibrated to withstand 1-in-200-year events – i.e., events in a year with 99.5% probability. The capital pool is funded from membership purchases and the purchase of NXM tokens for risk and claims assessment.

The minimum capital requirement (MCA) is currently 162,425 ETH, and is composed of two elements:

Best Estimate Liability (BEL) which represents the expected loss on each individual cover.

Buffer, which is made up of:

The Smart Contract Cover Module, based on the exposures that Nexus Mutual has to the covers it has written.

The Currency Module, which allows for possible fluctuations in the value of other currencies relative to the value of the base currency, ETH. The Currency Module which results in the lowest MCR% is picked.

The total MCR is calculated off-chain every day in order to save on gas costs, with the result notarised on-chain.

Asset Investment

An important part of an insurer’s responsibilities is to invest the assets they have in their treasury, to hedge their risk and earn returns on the reserves they hold. Since Nexus holds all its funds on-chain, it invests only in ETH and ERC-20 based assets. The investment process is automated via Uniswap and is purely buy-and-hold, with trades rebalancing the pool as required. Each asset has a minimum and maximum threshold, which represents the minimum and maximum units of any asset the mutual can hold.

The types of investments Nexus Mutual sees as appropriate are:

Staking ETH;

Investing in financial instruments based on collateralised lending;

Investing in interest-yielding decentralised money markets;

The DAI Savings Rate.

Nexus currently holds two investments: staked ETH from Lido Finance and a Maple Finance deposit.

Products ☂️

Nexus Mutual offers 4 core products. If a product has a high premium associated with it, it means that the project is either not seen as safe, or the demand for the cover is too low to stake NXM against it.

Yield Token Cover

Members using Convex Finance, Yearn Finance, Curve, and Idle Finance may want protection across multiple protocols. The product protects up to 90% of any loss that causes a yield-bearing token to de-peg from market value.

Protocol Cover

Protects against a hack on a specific protocol, such as code being used in an unintended way, economic design failure, oracle failure, governance attacks, protection for assets on L2s, non-ETH smart contracts, and a protocol across multiple chains.

Custody Cover

Protects against a custodian getting hacked where a user loses more than 10% of their funds or withdrawals from the custodian are halted for more than 90 days.

ETH2 Staking Cover

Provides protection against missed rewards and penalties incurred by validators, like missed consensus rewards because of being offline, and for periods post the Merge (i.e., now), any execution rewards missed as a result of being offline. Unless the periods of being offline are not extended or are lower than a constant number over a particular period (e.g., 12 hours over a 7-day period), this product could be gamed to save on validation.

The Trends Supporting Nexus Mutual’s Emergence 📈

There are two main trends that highlight the need for a protocol like Nexus Mutual, the first one stemming from issues with the current insurance industry, and the second from demand in the crypto ecosystem.

Firstly, insurers today decide how customer funds are handled – how it is invested, which risks it will back, and when it gets paid out to shareholders. Interests are not directly aligned since the insurer has unlimited upside, but the customer bears the brunt of the insurer going bust, like with AIG in 2008. There is also no real way for customers to judge how safe a particular insurer is. Moreover, 35% of premiums are lost due to legacy and bureaucracy issues with the system, in distribution, operational and regulatory expenses, capital costs, and profit. The on-chain nature of Nexus’ model, which provides transparency into how funds are managed, along with its governance and economic structures, alleviates many of the above issues.

Secondly, the crypto ecosystem has grown very quickly in a very short span of time. This has come with many growing pains, with the total amount lost from smart contract hacks according to Molly White’s (in)famous Web3 is Going Great reaching a staggering ~10.9 billion to date. Smart contracts get hacked for the most benign and avoidable reasons – look at Wintermute’s recent hack, for example. Users, protocols, and investors all need confidence that the projects they are investing in and building are safe and funds are protected. Hence, the demand for insurance for the protocols should be roughly correlated with the growth of the crypto ecosystem itself – an interesting dynamic which Nexus replicates, as we’ll touch upon later.

Launch & Future Roadmap 🚀

Launch

Nexus Mutual was launched in May 2019 with its first product, Smart Contract Cover (which has been discontinued since and rolled up into Protocol Cover) going live in July 2019.

Future Roadmap

Although Nexus’ roadmap has not been updated since December 2020, it has progressed on developing its core products, custody cover and yield token cover, while introducing ETH2 staking cover.

An interesting part of the roadmap is the ‘real-world products’ on the top right, such as earthquake cover. Nexus Mutual’s core structure enables it to be more cost and risk efficient than TradFi insurers, giving it an advantage. However, in order for this to be achieved at scale, adoption of crypto and DeFi rails by TradFi companies will have to reach a critical mass, which is still a while away.

Team 🤵♂️🤵♀️

Nexus Mutual’s core team has 7 members:

Hugh Karp, the founder, an insurance professional and actuary with 15 years of experience, including as CFO of Life Insurance, UK and Ireland, at MunichRe.

Kayleigh Petrie, who focuses on marketing, communications, and engagement.

Ricky Tan, a UC Berkeley MBA with experience in institutional finance and was founder of research company TokenData who runs Business Development.

Roxana Danila (former Tech Lead at Meta), along with Anatol Prisacaru, Dragos Horodnic, and Dan Octavian who have a combined 22+ years of experience, in the Engineering team.

The Advisory Board, which plays a key role in the governance of Nexus Mutual, comprises of:

Hugh Karp

Rennis Malbardis, an insurance expert who was Head of Finance Projects at MunichRe and Capital Solutions Actuary at Aon.

Graeme Thurgood, an insurance professional with 17+ years of experience in setting up and running mutuals in the UK, who previously worked at RSA, Allianz, and Aviva.

Roxana Danila

Nick Munoz-McDonald, a security expert who was previously Head of Audit for Solidified.

All in all, the team behind Nexus is composed of individuals with the right set of attributes to correctly guide and grow the mutual. The levels and specific areas of experience are well suited to Nexus’ needs.

Thoughts from Using the Protocol 🖱️

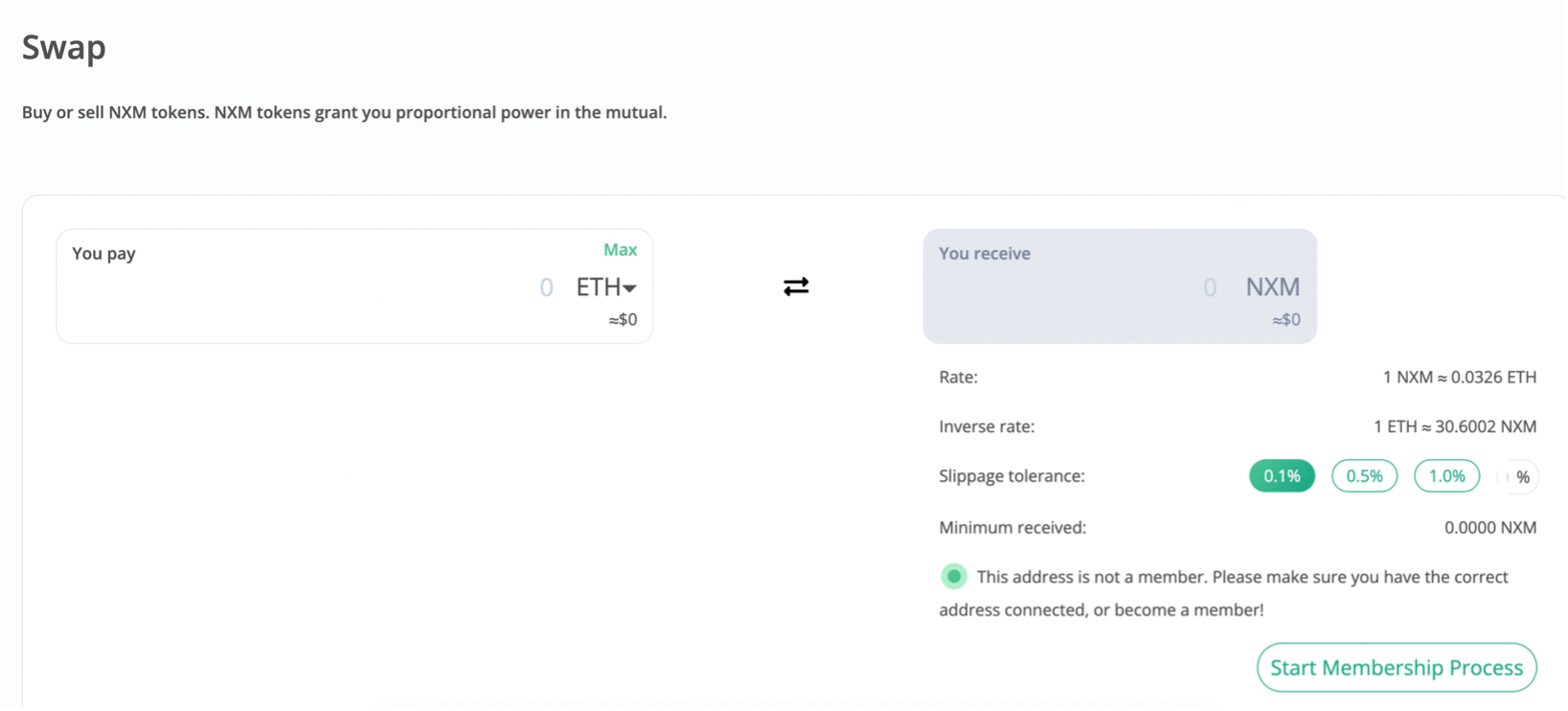

Nexus Mutual’s dashboard and layout are pretty simple to use. The token is self-contained within the Nexus ecosystem, which reduces the complexity of transacting with the protocol. Users just need to have ETH to buy membership and ETH or DAI to buy NXM tokens, which is straightforward enough.

As you can see above, any UI/UX issues are those endemic to Web3 in general – there is no explanation of what slippage is, for example. It is a good sign that the dashboard can immediately recognise whether the connected wallet is a member and if not, direct it towards starting the membership process.

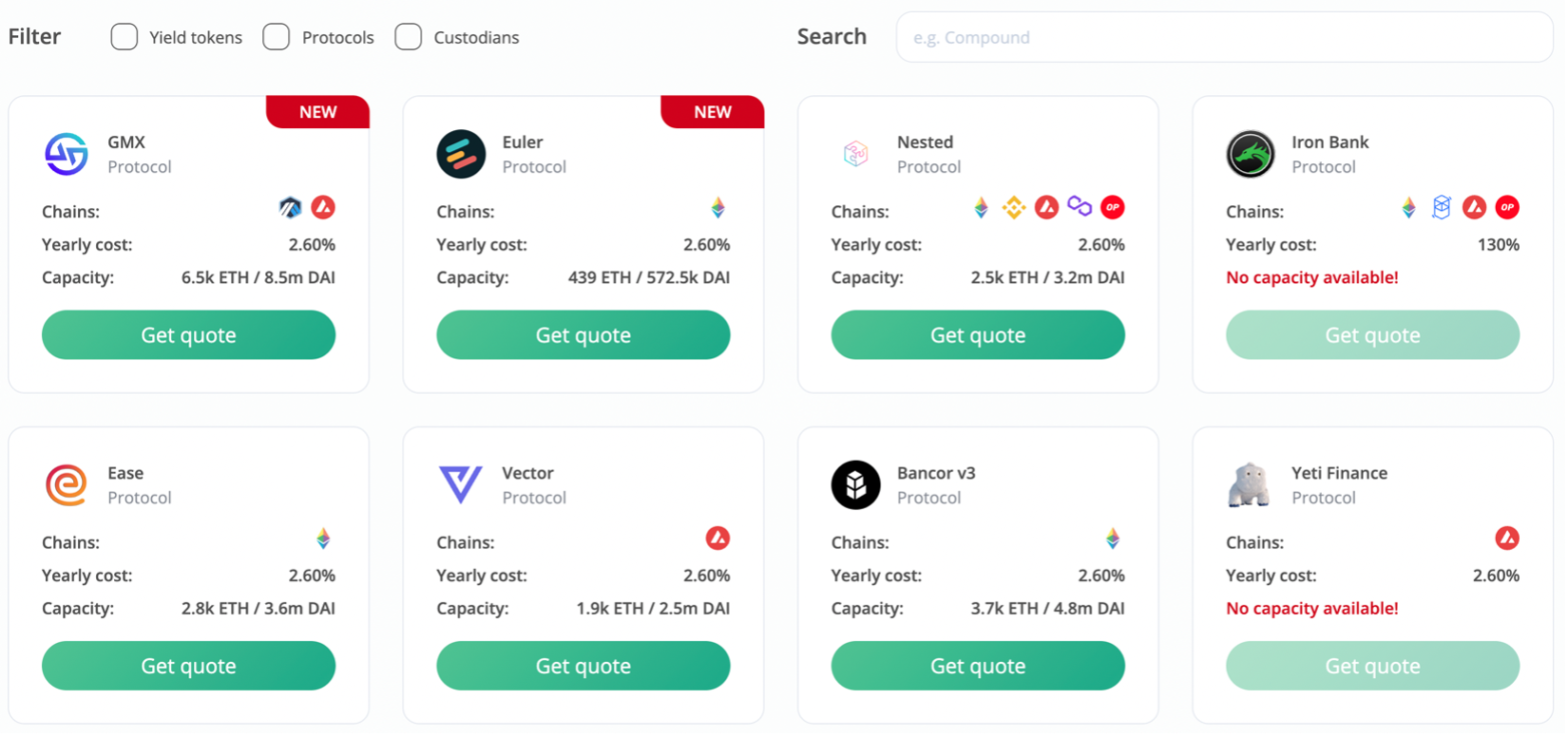

On the membership page, the agreement is clearly outlined, making it straightforward for members to join. Buying cover and getting a quote is also pretty easy, with the search and filter functions making it more user-friendly:

In summary, Nexus Mutual is well-designed and simple to use from a UX perspective, while its UI is clean and easy to navigate.

Tokenomics 💸

NXM, an ERC-20 compatible token, is the incentive mechanism that binds Nexus Mutual’s ecosystem together. As we have discussed above, the token primarily has 3 uses: to purchase cover, to assess risks, and to assess claims. It is also used as the main reward mechanism for members participating in risk and claims assessment and governance.

Token Price

The NXM token price is managed by Nexus via the token price model and adjusted according to the formula A + (MCR / C) × (MCR%)^4, where A and C are constant values that were calibrated at launch (0.01028 and 5,800,000 respectively), MCR is the minimum capital requirement, and MCR% is the ratio of the Capital Pool to the Minimum Capital Requirement. The token price is constructed to ensure that Nexus is flexible enough to react to market conditions – for example, when funding (essentially demand to purchase cover) is lower, price is lower as an incentive to purchase NXM tokens, while when funding is higher, the token price increases. The supply of NXM tokens is not fixed, but all methods of generating new NXM tokens require a contribution to the mutual – claims and risk assessment and voting in governance.

Given that NXM tokens are not tradable on any exchange and can only be used within the self-contained Nexus Mutual ecosystem, speculative mechanics do not impact token price. The only way for users to derive value from NXM tokens is by redeeming ETH from the mutual, which is how NXM holders achieve exit liquidity.

Redemptions

The trickiest (and most crucial) part of Nexus’ tokenomics flywheel is its redemption mechanism. While NXM can be redeemed for ETH from the capital pool, several restrictions apply to this, which are in place to ensure that the mutual always has sufficient funds to pay claims:

Redemptions are restricted if MCR% is < 100% (and purchases are restricted if MCR > 400%).

Redemptions and purchases are limited to 5% of the MCR per transaction.

The redemption price is set at 2.5% lower than the purchase price derived from the token model to discourage speculative buy/sell behaviour.

There is a minimum capital pool level set at 162,425 ETH, below which no redemptions are allowed.

Given that the current size of the pool is 153,772 ETH, and the pool size has either hovered around or been below the minimum level since December 2020, members have been stuck holding NXM and not been able to attain sufficient exit liquidity. The only way in which members can exit their NXM holdings is via wNXM (wrapped NXM), which is a 1-to-1 backed token that can only be generated by wrapping genuine NXM. wNXM is tradable on exchanges but cannot be used at all within the Nexus Mutual platform. Only members can wrap or unwrap NXM tokens.

There is a significant disparity between the prices of NXM and wNXM, since the latter is subject to demand and supply market forces, while the former is not. The price of wNXM is bound to be lower because of two reasons:

There is no other way for members to achieve exit liquidity, leading them to sell their wNXM at a discount.

The counterparties that buy wNXM do so for two reasons – speculation, or to receive a discount on purchasing NXM tokens. In the latter instance, wNXM token buyers become (or are already) members of Nexus Mutual, unwrap the tokens, and use it to purchase cover or participate in governance and claims and risk assessment.

Nexus’ redemption model is the cause of most of its problems. It disincentivises new memberships since members cannot obtain ‘true’ liquidity and rewards for participating in the running of the mutual, which is reflected in the very slow growth in new memberships – the number of holders has increased by only 29% since early 2021, which tracks much lower than the crypto ecosystem it should be heavily correlated with.

The importance of fixing the redemption mechanism and providing true exit liquidity to members is reflected in the number of exits seen in the ecosystem already. 25.7% of NXM tokens have been wrapped and the very fact that wNXM trades at such a discount to NXM price ($14.74 vs. $42.36) highlights how desperate members are to cash out their rewards. Furthermore, the 2.5% haircut applied on purchase price to disincentivise redemptions is also problematic; even though it is meant to encourage members to stay in the ecosystem, it may make potential new members wary of joining since their rewards from claims and risk assessment and governance need sufficiently account for this price disparity.

Governance ⚖️

Nexus Mutual’s governance model is one of the more developed ones we have seen to date. It does not go on the extreme end of decentralisation, recognising that the optimum way to run a growing decentralised business requires pockets of centralisation to enable scalability.

The Advisory Board, as mentioned above, is at the core of the governance process. It has no custodial rights over the funds in the capital pool and each board member can be replaced at any time. Nexus’ governance model is based on the following three principles:

High member participation, with the recognition that member attention can vary and gas costs for voting can be high and must be managed.

Minimise centralisation.

Avoid stagnation and still update the code and protocol even if member participation is low.

During the governance process, the board initially whitelists all governance proposals and provides a recommended outcome for each proposal. The proposal is then put to the entire member base for a token-weighted vote capped at 5% maximum weight per member. This reduces centralisation and whale risk, as does the fact that token rewards for voting are distributed as per the number of members voting, rather than the number of tokens voting. The majority outcome of the vote wins if the quorum of 15% is reached, otherwise the board recommendation proceeds. Tokens are locked for a period of time after participating in voting to ensure that voters have ‘skin in the game’. The board is also not unchangeable or immutable. Any member can raise a proposal to replace a board member with themselves, with the board having no input into this process other than voting as members themselves.

The governance solution is built on the GovBlocks platform, which allows for a modular governance approach where voting weights, quorum levels, rewards, and all other parameters can be changed if the member base proposes to do so. It also has an ‘automatic actions’ feature, which allows for automatic deployment of any feature changes agreed upon in governance – i.e., proposal results can be implemented automatically. This further increases speed and scalability and is a solution that other protocols should emulate. However, a point of concern is that GovBlocks currently does not have a website, its Twitter page only has 340 followers, and the website link on Twitter now redirects to ‘PlotX’, which is completely unrelated to governance and is a crypto-based fantasy trivia game. It would be good for Nexus to update their documentation and confirm whether they are still using GovBlocks.

Two of the major decentralisation trade-offs highlighted are:

Emergency Pause Function, where all board members can stop all transactions. This is a centralisation risk and while the board has agreed that this will only be used in emergencies, it requires members to inherently trust the board. If it is used incorrectly, however, the board member removal process enables accountability for members.

Off-Chain Capital Model and Pricing Computation, where the capital and pricing models are run off-chain to save on gas costs. As L2 scaling solutions grow in maturity, Nexus could potentially conduct these computations on-chain for greater transparency.

Nexus’ entire governance process is well-constructed and well thought out. Centralisation is dampened as much as possible while still ensuring decision-making speed and scalability of the protocol. It is important to recognise that maximally decentralised organisations have the benefit of total egalitarianism, but also prevent scalability and in many cases can increase stagnation. The use of the GovBlocks platform also shows how Nexus Mutual values speed and growth, and that the modularity of the solution recognises that protocol governance is ever-changing.

Traction & Performance 📉

The active cover amount today is 145,777 ETH while the capital pool amount is 153,772 ETH. The minimum capital requirement is 162,425 ETH, which means that the capital pool needs to grow now since it is getting much closer to the active cover amount than it ideally should, putting Nexus at danger of not being able to cover its claims.

The losses experienced compared to total premiums paid are 34% (claims accepted/total premiums paid, $7.6 million/$22.4 million). This is extremely high, especially when you consider the premiums earned in 2022 ($5.7 million) and claims paid out in 2022 ($5.4 million), which is staggering. This highlights the amount customers are paying for premiums and the general level of demand in the market, but also the number of hacks/smart contract failures that have occurred this year. However, this number may be significantly distorted by the $4.995 million paid because of the Rari Capital hack, which accounts for 65.7% of total losses and 92.6% of 2022 losses. The premium for this Cover ID (7149) was $10,676.55, with the cover start date of 4th April 2022 and the pay-out date on 18th May 2022. The premium was not paid for very long and the hack took place not long after the cover was taken. Assuming the premium was paid daily, the yearly premium was only 1.77%, which seems to be very low. This shows the confidence that risk assessors had in Rari Capital and demonstrates the danger and immaturity in crypto and DeFi in its current state, where even contracts and pools deemed to be ‘safe’ can still be so risky and lead to such a large loss for the mutual.

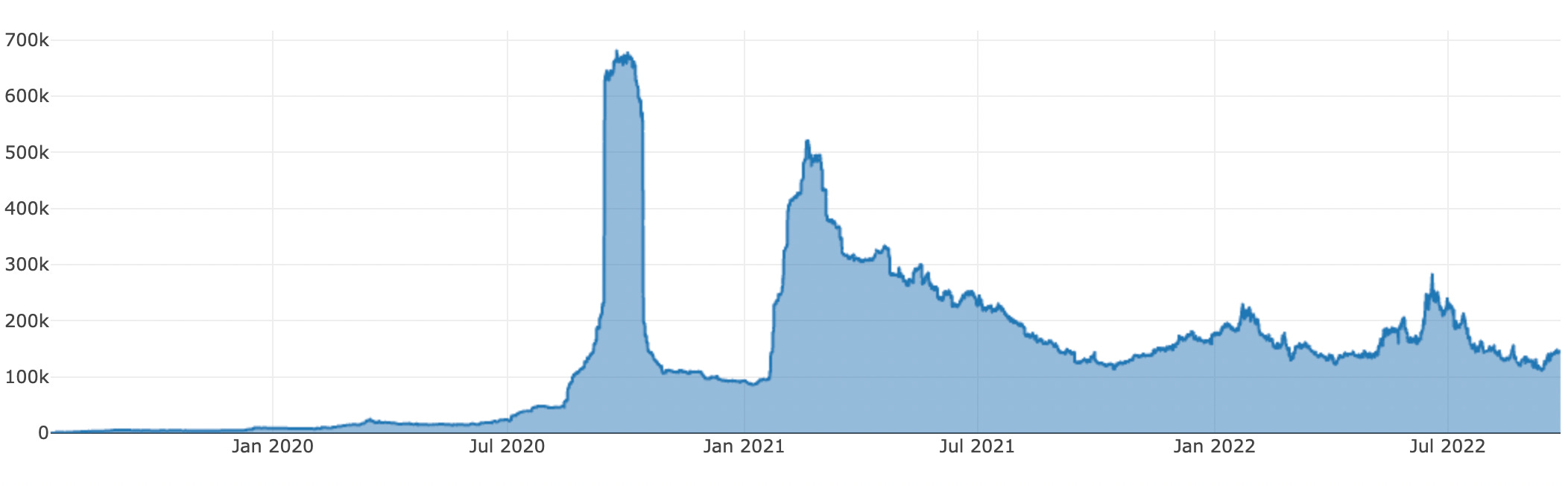

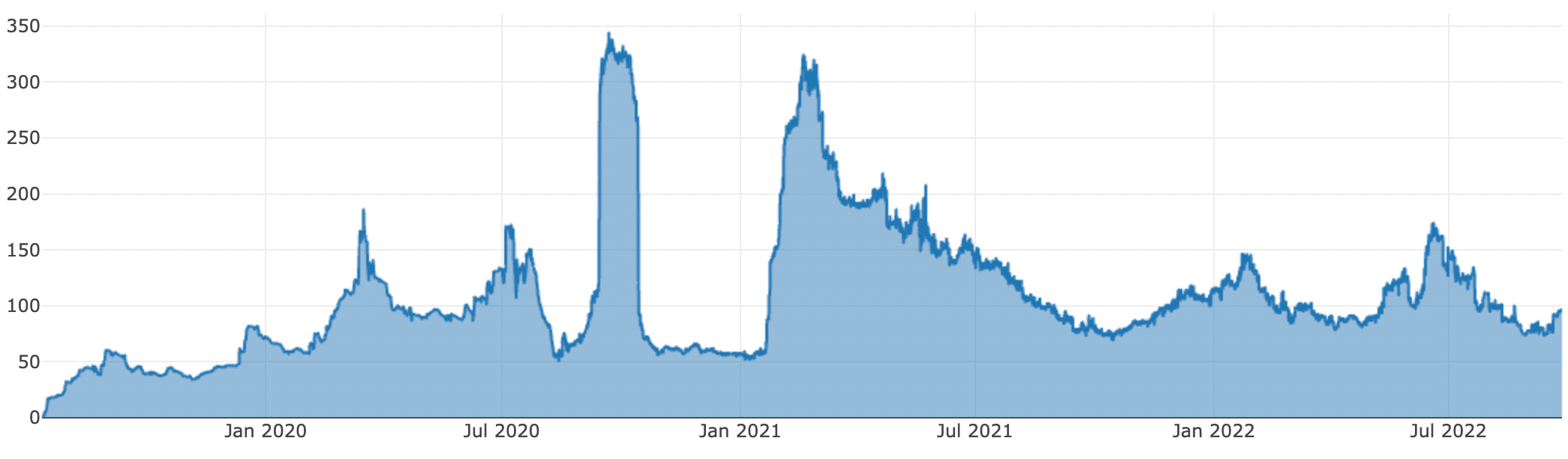

As can be seen above, active cover has been on a downward trend since February 2021 and even more from its peak in summer 2021, reflecting the broader downturn in DeFi – with less funds in projects to insure, active cover is bound to fall. This tracks the dynamic we mentioned above, wherein the success of Nexus Mutual is positively correlated with the success of DeFi. When there are more projects to insure, there is more cover in force and there are more premiums to be paid.

The market cap of NXM in the market is $42.8 million, which is much lower than the amount in the Capital Pool. However, redemptions are halted right now which means that there is no real value to holding the NXM tokens other than staking them in the hope that the capital pool rises high enough to enable redemptions. Since the Pool is lower than the minimum capital requirement right now and considering the depths of the current bear market, redemptions will probably lag market recovery and be enabled after it is clear that the market has recovered. This means that, currently, the value of the NXM token is only to purchase cover and given how demand for active cover has been steadily decreasing since February 2021, demand for the token would probably not be high. Moreso, since wNXM can be purchased at a discount on the open market, value can leak from the Nexus ecosystem and further reduce demand for natively buying the NXM token.

The above graph demonstrates the capital efficiency ratio for Nexus Mutual, which has fluctuated between 77%-100% since August 2022 and is at 95.76% as of September 26, 2022. However, since the capital pool size is already below the minimum capital requirement, Nexus needs to incentivise the injection of liquidity into the capital pool by lowering token price even more. This disadvantages current NXM holders but may be the only way to shake the paralysis that Nexus is in, attract capital, and grow in the bear market.

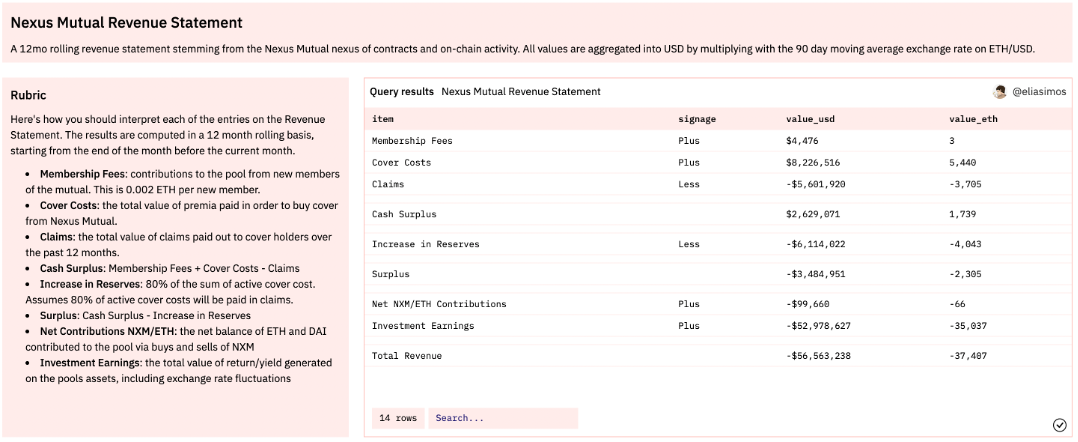

Lastly, the above 12-month rolling revenue statement indicates that Nexus Mutual has made heavy losses of $56.5 million over the last year, of which a humongous ~$53 million can be attributed to losses in investment earnings, i.e., losses stemming from investments. This tracks with the wider bear market but can also showcase that Nexus needs to invest in uncorrelated assets like Goldfinch loans to survive the bear and come out stronger. A positive sign is that they seem to have realised this, having invested in Maple Finance loans as of August 2022. Only 20% of the ETH in Nexus’ capital pool was earning interest as stETH when the Maple proposal was approved, which is capital inefficient and places Nexus’ funds at risk.

Concerns & Headwinds 🤨

Some concerns include:

The broken redemption mechanism. Once this is fixed, the growth prospects for the protocol are high.

Its investment returns, which should be much more capital efficient and deployed in uncorrelated assets to weather risky situations like the current bear market.

The documentation has not been updated since December 2020 and prospective members should have access to updated information – a case in point is the confusion around the GovBlocks mechanism that has been used.

A few headwinds could include:

The KYC process, which, although is necessary and enables the tokenomics and governance of the protocol to flourish, may disincentivise crypto natives who are wary of KYC to participate. This, however, is unavoidable and can only be changed when robust forms of on-chain identity have matured enough.

Competing protocols like Unslashed Finance and Sherlock DeFi which are selling their products directly to protocols and grabbing market share from Nexus.

Potential clones on other blockchains, such as Soteria on Binance Smart Chain. However, Nexus being built on Ethereum and having an avenue to expand to other users and cut costs via L2s dampens this risk.

Closing Thoughts ⌛

Nexus Mutual is a well-constructed protocol with a robust governance system and a well-defined tokenomics model that is mainly hampered by its broken redemption mechanism. Once this is fixed and the protocol figures out how to attract more users to its platform and de-correlate away from the wider DeFi and crypto market by offering insurance for real-world products (like earthquake insurance, as stated in its roadmap), the potential for Nexus’ future growth is unlimited.

Disclaimer

This is a personal blog. Any views or opinions represented in this blog are personal and belong solely to the article authors and do not represent those of people, institutions or organizations that those authors may or may not be associated with in professional or personal capacity, unless explicitly stated. All content provided on this blog is for informational purposes only. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

👇🏽 please hit the ♥️ button below if you enjoyed this post.