Introduction 👋

This is the fifth article in our Protocol Analysis series. In this series, we use our investment template outlined in How to Analyse a Web3 Protocol to fundamentally and critically analyse a variety of crypto protocols, aiming to separate the ‘real’ from the hype. Let’s dive in!

Protocol: GMX, a decentralized spot and perpetual exchange that was built on Arbitrum (Layer 2 Ethereum scaling solution) and then Avalanche (AVAX) with plans of launching on other chains in the future. Since GMX is decentralised, all trades are executed entirely on-chain through wallets with no need for KYC.

Overview of GMX 🗒️

GMX allows users to trade spot markets for certain assets as well as trade perpetual swaps (perps) using leverage up to 30x. GMX has a pool of assets known as the GLP pool through which spot and perp trades are executed. Liquidity providers who deposit into GLP pools earn fees from market making, swaps, and leveraged trading.

One of GMX’s defining features is its unique oracle pricing method which enables extremely low slippage. The pricing is dynamic and is supported by Chainlink Oracles and aggregated prices from exchanges like FTX and Binance. We’ll dive further into GLP pools and the oracle pricing method below.

Another aspect that stands out is that GMX has had no VC fundraising. It started life out as Gambit Protocol on Binance Smart Chain and had two native tokens – GMT and XVIX. The raise for these two tokens was from the public community.

How Does GMX Work? 🤷

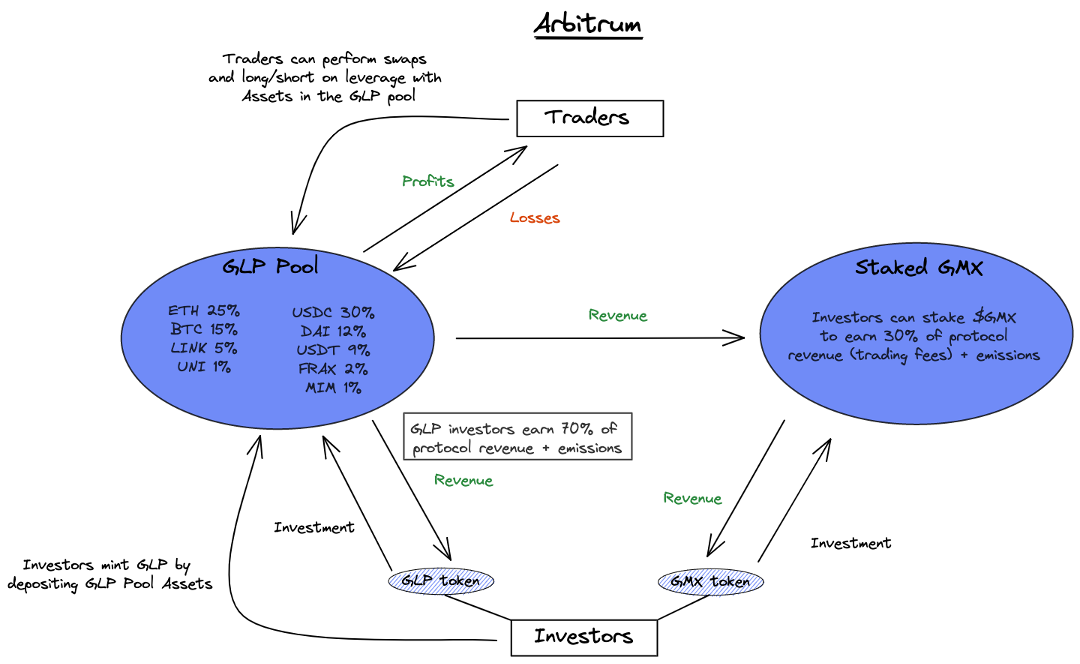

GMX has a two-token model: $GMX and $GLP. Let’s start with liquidity providers and GLP.

Users can deposit liquidity into a pool of supported assets with any one of the assets, and then mint GLP tokens which represent their share of the GLP pool. They can also redeem any assets by burning their GLP tokens. The versions of GMX on Arbitrum and Avalanche have two separate GLP pools with differing constituent assets – ETH, BTC, LINK, UNI, USDC, USDT, DAI, and FRAX on Arbitrum, and AVAX, ETH, BTC, and USDC on Avalanche. The Arbitrum and Avalanche versions work in exactly the same way, with the assets being the only difference.

Given that the value of the GLP token changes depending on how the value of the index assets inside the GLP pool change, the GLP pool essentially mimics an index fund of high-quality crypto assets. The GLP pool also serves as a counterparty for traders using the GMX exchange to perform spot and perp trades. Let’s break this down further. When traders open leveraged positions on GMX, they use assets within the GLP. For example, if a trader wants 2 BTC worth of leverage, then 2 BTC is ‘rented out’ from the GLP to the trader to give them their exposure. Therefore, if the trader makes a profit, BTC is withdrawn from the GLP and paid to the trader as profit. It can hence be deduced that GLP holders essentially lose money when traders make profits and make money when traders make losses.

The fees associated with minting GLP tokens using a certain asset depend on which of the assets in the pool are underweight or overweight. If, for example, ETH is underweight in the pool, the fees for minting GLP using ETH are lower, thus incentivising ETH to be added to the pool. The weights are also adjusted to help GLP holders hedge against traders’ open positions. If more traders are long LINK, the pool has a higher LINK weight, and if open positions skew short, the pool increases its proportion of stablecoins to protect downside. All of this results in GLP being one of the more ‘stable’ indices in crypto, with downside and upside both minimised.

GLP holders make fees from market making, swap fees and leveraged trading. All fees are paid out in ETH on Arbitrum and in AVAX on Avalanche, hence giving LP’s and GMX holders ‘real yield’. The trend of real yield has really caught on, especially following the Terra crash and 3AC, Celsius, and Voyager implosions. Giving users profit in more widely transacted tokens such as ETH is a positive sign for user retention.

This entire process can be summarized with the amazing diagrams made by @RileyGMI in his post about GMX:

Staking GMX earns 30% of all fees on both Arbitrum and Avalanche plus emissions and ‘multiplier points’, which we’ll explore further in the Tokenomics section below – the Escrowed GMX model is particularly interesting. GLP holders, meanwhile, only earn 70% fees from the specific chain from the above two that they have been deployed on. GMX stakers face much lower risk than GLP holders, who also have to bear the risk of losing some value in both bull and bear markets. As these two tweets from @FloodCapital summarise:

GMX’s product is also geared squarely towards traders. The protocol is able to offer low slippage and fees. Low slippage is achieved by using an oracle pricing model instead of the typical AMM model used by most DEXes. This oracle pricing model uses Chainlink to source the prices of supported assets from top centralised exchanges which leads to more accurate price discovery. This also means LP’s don't suffer from impermanent loss which is a huge step forward in protocol design. In the AMM model, since they use an x*y=k model of pricing an asset, it can lead to huge slippage as there is a need for LP’s to constantly conduct arbitrage trades to ensure the price is as close to market price as possible. This also reduces the risk of liquidation significantly since prices do not sometimes arbitrarily ‘bounce’ – go down and back up quickly, which triggers automated liquidations even when the ‘true’ price did not fall as much.

GMX charges a trading fee of 0.1% when opening and closing a position. Traders also pay a ‘borrow’ fee to the GLP pool every hour, which varies according to pool utilisation.

The Trends Supporting GMX’s Emergence 📈

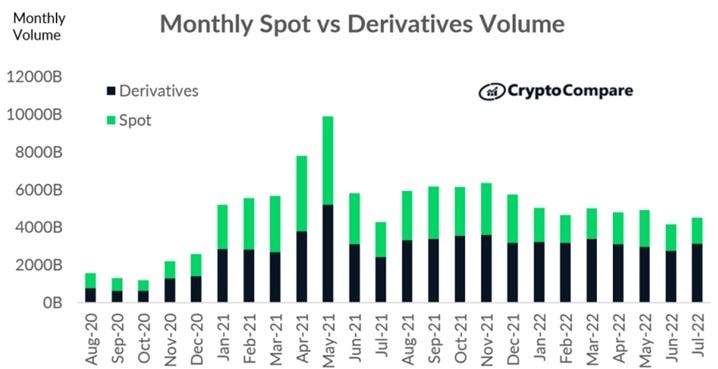

According to the BIS, the market value of all derivatives contracts is worth $12.4 trillion in 2021, and the total notional amounts outstanding for contracts in the derivatives market is estimated to be $600 trillion. In US equity markets, options volume is 35x spot volume. In crypto markets, derivatives volumes are 2.24x spot volume on centralised exchanges, indicating quite some room for growth even if you think crypto’s growth prospects aren’t very high (which, well, you hopefully don’t if you’ve been reading this newsletter).

DEX volumes are much lower – Binance itself accounts for 46.7% of total futures volumes, and Deribit has 90% of Bitcoin options volumes. There is a lot of open space for decentralised derivatives markets to grow in, and GMX and other protocols like Dopex, Katana, and Ribbon have recognised this. The below image is Jump Crypto’s market map, and GMX would be a decentralised perpetual options and futures exchange, with the (huge) added benefit of also being a spot exchange. As a side note, it’s interesting to see this map (from January) doesn’t include both Dopex and GMX, the two most successful decentralised options protocols, highlighting how early in its evolution this market is.

The growth in overall DEX market share is reflected in the top 10 spot DEXes increasing their quarterly volume by 441.92% from Q1 to Q4 2021. The top 10 DEXes now make up 9.05% of all trading volume, up from just 1.67% in Q1 2021. Total DEX perpetual volume market share also increased from basically zero to ~3%. DEX spot and perp market share has grown significantly this year, primarily due to better UX, more projects tackling different corners of the market, reduced gas fees due to lower demand on ETH Mainnet and improvements in L1 and L2 scaling solutions.

GMX has also chosen to build on Arbitrum, one of the premier L2s for options protocols – Dopex is built on Arbitrum as well – and the largest L2 by market share. Arbitrum has high throughput, and its Nitro upgrade promises faster transactions and lower fees by compressing 7x more transactions into a block. Options contracts need accurate pricing and sub-second confirmations, making throughput paramount. This can explain the relative trade-off they have made in decentralisation, with Arbitrum’s solutions not being decentralised yet (although they have indicated this is being actively worked on). Avalanche fits the same bucket, with its subnets (application-specific chains), rollups, and tech being a draw for an options protocol.

Launch & Future Roadmap 🚀

Launch

Gambit Protocol’s two native tokens, GMT and XVIX, were merged, migrated, and then swapped to GMX when the protocol launched on Arbitrum. 6 million of the forecasted maximum supply of 13.25 million GMX are from the GMX migrated over from Gambit Protocol.

Future Roadmap

For now, GMX plans on focusing on perfecting the platform on Arbitrum and Avalanche. They then plan on deploying their smart contracts on other chains. They haven’t indicated which ones yet, but a best guess would be other Ethereum L2 scaling solutions such as Optimism as well as alt-L1 chains with high throughput that are EVM compatible such as NEAR Protocol, since derivatives markets need less-fragmented liquidity and faster, more accurate transactions.

One of the more interesting aspects of GMX’s roadmap is X4, a ‘protocol-controlled exchange’. From their announcement post:

With X4 we propose to build an AMM that gives pool creators and projects full control over the functions of its pool. This means that when a pool is created, the creator can specify any custom behaviour that they would like on adding liquidity, removing liquidity, buying, and selling.

Some of the benefits include:

Dynamic Fees where projects can set fees to any percentage they prefer, fees can be changed easily, different fees can be charged for different actions, and fees adapt to specified parameters.

Access to more tokens with customisable bonding curves.

Better composability and flexibility, e.g., pools can create yield-bearing tokens.

DEX aggregation, which could be a huge unlock for liquidity.

For further details, check this thread out:

Team 🤵♂️🤵♀️

The team of 11 behind GMX is completely anonymous and includes:

4 Developers – xdev_10, gdev8317, xhiroz, vipineth

1 Designer

3 Marketing, BD & Partnerships – Coinflipcanada, puroscohiba, bagggDad

3 Community Managers – y4cards, supersonicsine

Hence it is tough to judge the credibility of the team. But by looking at the product they have built to date, we can be reasonably certain of its legitimacy. Moreover, there is a community of developers building on GMX – for example, GMX Analytics was built by @cryptomessiah, while @marcus.crypto built the GMX Returns Calculator. This adds enough confidence in the protocol and team as well.

As mentioned above, they have also not raised any VC money, instead opting for a bootstrapped approach. VC funds that wanted to invest had to do so on the open market like the rest of us (big win!).

Thoughts from Using the Protocol 🖱️

The protocol has an extremely clean UI and connected to our wallet with no issues. Different types of trades such as spot and perp are made very clear. Features like liquidation price, entry price, exit price and fees paid are also very easily accessible.

The process of buying GMX or GLP using any of the assets above is also pretty straightforward – click on Buy and simply swap the asset for GLP, with fees being clearly listed. The ‘Save on Fees’ feature is also pretty useful and helps endear users – the amount of GLP to be purchased just needs to be entered in the order form, and fees per asset are displayed. This is also very useful as an incentivisation mechanism for users to deposit underweight assets and not deposit overweight assets.

All in all, the UI/UX is pretty simple and intuitive with all the relevant information clearly displayed.

Tokenomics 💸

GMX is the protocol’s utility and governance token. GMX has a forecasted maximum supply of 13.25 million tokens, which can be increased if there are more products launching and liquidity mining is required, but this will be subjected to a governance vote before any changes are implemented.

The GMX token primarily accrues value by earning 30% of all fees and distributing them to stakers, along with token emissions in ‘esGMX’ (escrowed GMX) that further incentivise holding/staking. The token is also used to vote on governance and determine future rules and goals of the protocol, such as esGMX emissions. Rewards from staking GMX are intended to provide long-term incentives for GMX holders to stake their coins and compound their rewards. GMX has also hinted at the possibility of stakers receiving fee discounts on trading, depending on how much GMX they stake.

Two key aspects to analyse in terms of value accrual are Escrowed GMX and Multiplier Points, while another special feature of the GMX token is its Floor Price Fund. Let’s take a closer look at these.

Escrowed GMX

Escrowed GMX, or esGMX, can be used in two ways:

Staked for rewards similar to regular GMX tokens;

Vested to become actual GMX tokens over a period of one year.

Each staked esGMX token will earn the same amount of esGMX and ETH / AVAX rewards as a regular GMX token. esGMX is not meant to be transferable unless a full account transfer is completed.

esGMX tokens can be converted into GMX tokens through vesting. When vesting is initiated, the average amount of GMX or GLP tokens that were used to earn the esGMX rewards will be kept in reserve. For example, if a user staked 1,000 GMX and earned 100 esGMX tokens, then to vest 100 esGMX tokens, 1,000 GMX tokens will be reserved. Note that this is an example, and the actual ratio depends on the average staked amount and rewards earned for the user’s account.

Some other key points around esGMX vesting:

esGMX tokens that have been unstaked and deposited for vesting will not earn rewards, while staked tokens that are reserved for vesting will continue to earn rewards.

After initiating vesting, the esGMX tokens will be converted into GMX every second and will fully vest over 365 days in a drip-feed manner. esGMX tokens that have been converted into GMX are claimable at any time.

Tokens that are reserved for vesting cannot be unstaked or sold. Partial withdrawals are not supported, so withdrawing will withdraw and unreserve all tokens as well as pause vesting. All esGMX tokens that had been vested into GMX will remain as GMX tokens.

Because stakers receive esGMX as a reward for staking, they are incentivised to stake that esGMX rather than vest it, since the process of vesting as described above is illiquid, requires a lot of capital, and takes a long time. Restaking esGMX is the logical move since rewards from staking esGMX are higher than the GMX received when vesting esGMX. This therefore makes sure that as much GMX/esGMX emitted as rewards goes right back into the system via staking, reducing sell pressure.

To summarise, value accrues to GMX from esGMX in the following ways:

esGMX received as staking rewards are incentivised to be restaked rather than vested, reducing sell pressure;

Vested esGMX releases GMX in a drip-feed fashion, reducing concentrated sell pressure;

2 million GMX have been allocated for esGMX emissions, but it is unlikely that these will all be released in the near future, which reduces supply inflation and therefore sell pressure.

Multiplier Points

Stakers also get multiplier points as a format of rewards without increasing inflation. Staked GMX receives multiplier points every second at a rate of 100% APR. The multiplier points are then staked, with each point receiving ETH/AVAX as a normal GMX token. Unstaking GMX/esGMX means that multiplier points are also burned proportionally – if, for example, 1,000 GMX is staked and 200 multiplier points have been earned, then unstaking 200 GMX would burn 0.2*200 = 40 multiplier points.

Floor Price Fund

This fund is denominated in ETH and GLP and grows in two ways:

GMX/ETH liquidity is provided and owned by the protocol. Therefore, the fees from this trading pair will be converted to GLP and deposited into the floor price fund.

GMX has partnered with Olympus to sell GMX WETH bonds. 50% of the funds raised from the Olympus bonds will be used to buy back and burn GMX as per the floor price fund. The other 50% raised will fund GMX marketing.

The floor price fund helps to ensure liquidity in GLP and provides a reliable stream of ETH rewards for those who staked GMX. As the floor price fund grows, it can be used to buy back and burn GMX if:

(Floor Price Fund / Total GMX Supply) < Market Price of GMX

Value Accrual

Multiplier points, the design of the esGMX system, and the 30% fees distributed from both Arbitrum and Avalanche deployments all act as sinks for GMX/esGMX and are meant to incentivise staking or, essentially, lock supply up longer-term. This method seems to have worked, with 86% of all GMX staked at an APR of 14.08% on Arbitrum without applying multiplier points, so the overall APR would be >20%, increasing demand for the token. The APR for GLP is ~29%, which is primarily made up of the ETH/AVAX earned from fees plus esGMX emissions, making this token very valuable to hold as well.

A summary of rewards and mechanics are:

GMX: earns ETH/AVAX, esGMX, and multiplier points when staked;

esGMX: earns ETH/AVAX, esGMX, and multiplier points when staked;

Multiplier Points: earns ETH / AVAX when staked leading to higher ETH/AVAX APRs;

GLP: earns ETH/AVAX, esGMX, and is automatically staked on mint.

Token Distribution

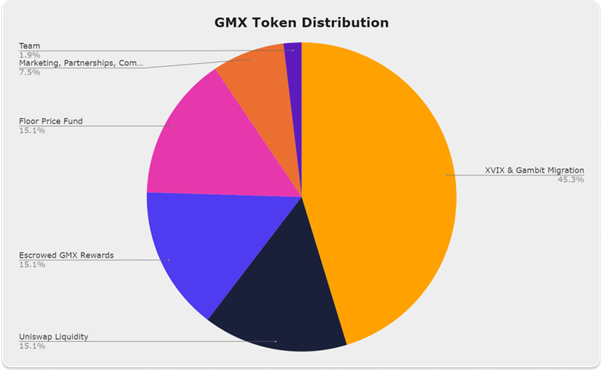

The 13.25 million of GMX will be distributed in the following manner:

6 million GMX from the XVIX and Gambit migration (45.3%)

2 million GMX paired with ETH for liquidity on Uniswap (15.1%)

2 million GMX reserved for vesting from Escrowed GMX rewards (15.1%)

2 million GMX tokens to be managed by the floor price fund (15.1)

1 million GMX tokens are reserved for marketing, partnerships, and community developers (7.5%)

250,000 GMX tokens were distributed to the team linearly over 2 years (1.9%)

The team has received a measly 1.9% of GMX supply, going a long way in embedding confidence in the protocol and the anon team.

The fact that the protocol has also bootstrapped itself and not raised funds from investors and therefore not diluted supply leaves them with a lot of room for token emissions to bootstrap usage.

2 million tokens have been allocated for the Floor Price Fund. The team does not intend to release them onto the market in order to avoid dilution of GMX holders.

There are 2 million GMX tokens allocated to esGMX emissions. The total amount of emitted GMX is likely to be lower than this, at least in the near future, since the GMX only gets released onto the market when holders lock their GMX/GLP in reserve for an entire year. Moreover, since all the GMX is emitted only after a year for each user, this reduces concentrated sell pressure and hence a downward impact on price.

GMX tokens are released non-linearly from esGMX emissions, ensuring that supply will likely not reach 13.25 million and hence protects token price from being impacted negatively by inflated supply.

Governance ⚖️

While the GMX token is meant to be used for governance, not much information (essentially none) has been provided on GMX’s governance procedures. It can therefore be assumed that a one-token-one-vote model has been implemented, which has a lot of flaws, as we’ve discussed previously.

Traction & Performance 📉

Total revenues are at $78 million since launch in August 2021. As of September 2022, GLP holders have earned a total of $54 million, while GMX stakers have earned $24.1 million in revenue. Supply-side revenue refers to fees earned by GLP holders while protocol revenue is that earned by GMX holders.

Monthly revenue has stayed relatively consistent since Jan 2022 (min of $6M and max of $9.9M) in the midst of the bear market, indicating sustained demand for GMX and the perps it offers.

Total cumulative volume on Arbitrum has reached ~$12 billion to date, with swaps accounting for $2.67 billion of that volume and swap fees totalling $6.9 million. Total AUM of the protocol has been on a consistently upwards trend and has reached $276 million to date, increasing by ~168% YTD. The total number of users has reached 98,862, increasing by a massive 760% since May 2022.

Traders have cumulatively lost more than they have earned in profit. This is important to track since it indicates that GLP holders have not lost out due to traders making profits. This is consistent with other perp exchanges, making it potentially profitable long-term for GMX since its model is negatively correlated with traders’ positions.

Another extremely bullish sign is that to date, GMX’s token incentives have actually been much lower than its protocol and supply-side revenue – $68.5 million in incentives compared to $78.1 million in revenues. This makes GMX one of the few protocols that actually have a legitimate profit margin at such an early stage, an absolute rarity in this market.

Trading volume has also rocketed upwards since launch. Volume has jumped by 309% between January and September 2022, reaching a cumulative total of $45.8 billion. Fees have also reached a total of ~$62.5 million since launch.

Overall, performance has been extremely strong, in terms of fees, total users, volume, and most other relevant statistics.

Gaps in our Analysis 🕳️

The main gap in our analysis is undoubtedly the Governance aspect, on which a lot of information is not readily available.

If any readers have further details on GMX’s governance model, feel free to reach out to us!

Suggestions & Closing Thoughts ⌛

The decentralised crypto derivatives market that GMX operates in (and arguably leads) is in its very infancy. GMX has charted a path forward for other decentralised derivatives protocols to follow, with its metrics, tokenomics, team, and product development all being top-notch to date.

The protocol has two primary risks:

The GLP pool can get depleted significantly if traders are profitable. GMX has mitigated against this by adjusting token weights depending on traders’ open positions, and the fact that historical data (admittedly not comprehensive) has shown that taking opposite positions to traders’ positions on perp exchanges is profitable.

In a bear market where trades skew short and make money, GLP pays out stablecoins to traders as profits while the index assets decrease in value. This can potentially be mitigated by a model akin to funding fees, as suggested by @FloodCapital again:

Another point to be aware of is the absolute lack of information given about governance processes. If GMX is to be a successfully decentralised protocol, this is a crucial component that requires a lot of attention.

All in all, GMX’s track record to date and the sheer size of its target addressable market makes it a no-brainer to keep a very close eye on this protocol, track its development and innovation, and use many of its features as templates for other derivative and DeFi protocols to emulate.

Disclaimer

This is a personal blog. Any views or opinions represented in this blog are personal and belong solely to the article authors and do not represent those of people, institutions or organizations that those authors may or may not be associated with in professional or personal capacity, unless explicitly stated. All content provided on this blog is for informational purposes only. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

👇🏽 please hit the ♥️ button below if you enjoyed this post.